Is anyone else annoyed by the advice that young people should give up hope of paying their own mortgage for their own home in favor of paying their landlord’s mortgage via rent? “People need to shift the idea that to be successful you have to own a home. It’s just not going to be in the cards for some people, and they’re in a worse position for trying to own a house,” she said.”

I say that instead of telling young people to give up on goals we should, as a nation, protect owning a home as if it was a basic necessity and do something about large %'s of homes/condos being owned by investors. It was possible to buy a home on a single income just a few generations ago. I’m sure it can be again if we make housing security a priority.

I’m in the process of buying my first house, and I’m pretty sure I’m putting more down than my parents paid for their whole first home.

I bought in 2019 and my down payment was half of what the house originally sold for in 2009. We’re all fucked.

Then they go on to say that home ownership is one of the primary forms of wealth accumulation in Canada like two sentences later. If you read between the lines a bit, the implication is that younger generations will have to work until they are in the grave.

Not too long ago, the tradeoff of renting was that it was cheaper, you didn’t have to care about repairs (in theory) and could take the money you saved to invest.

The rental market is so outrageously out of whack that it is no longer the case. If you don’t own your home, you’re paying for someone else’s mortgage, while not having the benefit of paying less to invest more. And that’s not even broaching the subject of slumlords and overall bad landlords.

I don’t think that’s the advice. Rather that renting can be significantly cheaper and less risky to your savings in the current market. Here’s an anecdote from where I live. If you were to buy the unit I live in today, you’d have to pay $3700/mo in mortgage, $1000 in maintenance, and $250 in taxes. That’s $4950/mo to “own” this place. Instead you could rent it for $3200. That’s $1750 difference. That’s a lot more than what’s going to be going towards your principal, your equity in the purchase case. Out of the $4950/mo, only $860/mo would be going towards equity. Everything else goes in someone else’s pocket. The renter would be able to stash more money than you till your 13th year in the mortgage. If this is the reality you’re looking at renting is significantly cheaper. I think that’s what the advice is about.

You’re ignoring the fact that the house is appreciating in price more than $1750x12 per year. In fact, my house has appreciated around $500,000 in the 3.5 years since I bought it, which is about $12,000 per month. Plus I get the principal amount I’ve paid in back on top of that.

So while it’s cheaper every month to rent and they do have more cash in their pocket today, it’s FAR better financially to own. I will be able to retire easily with a paid off mortgage and very low living expenses, a renter may never have enough cash saved to be able to retire at market rental rates even if they put every single dollar they save each month away.

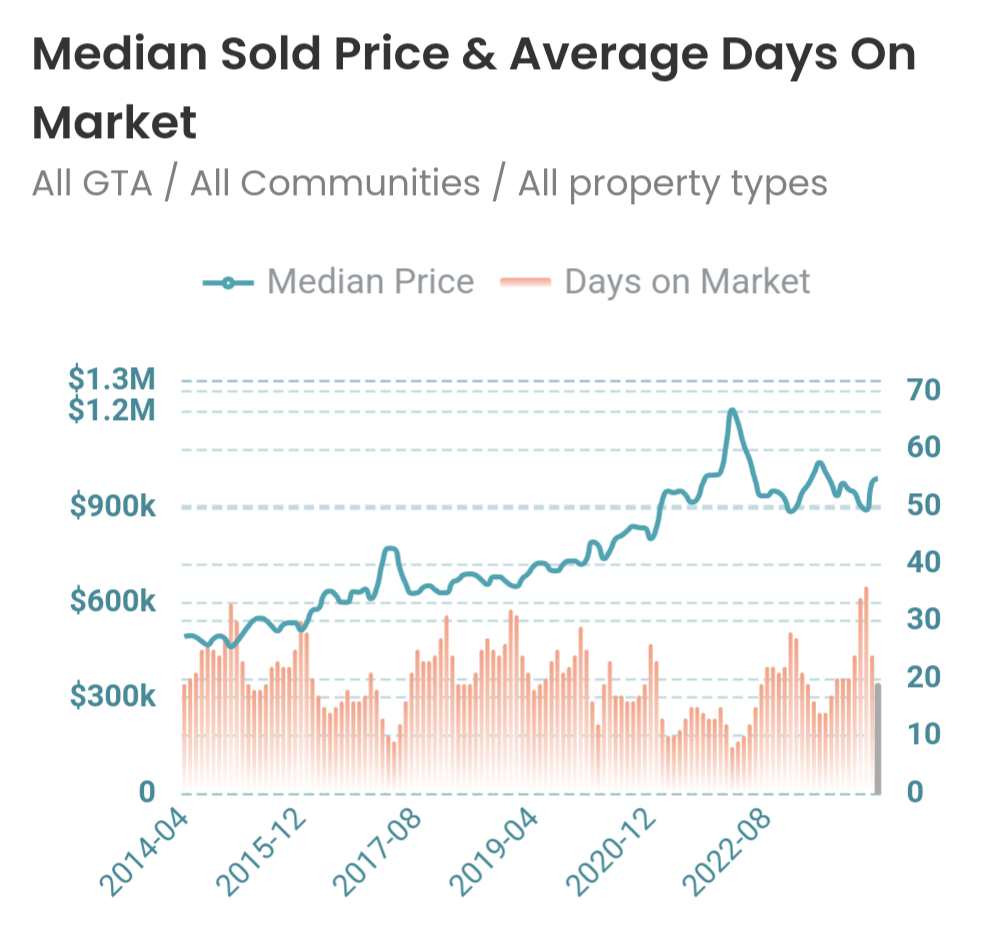

This is true if it-only-goes-up. Prices in the GTA for example have been flat since they came down from the peak in 2022:

So I’m only ignoring price appreciation because not all markets in Canada are upwards moving and I’m not betting it’s gonna go up or down.

If you bought at the peak then lost your job and had to sell you’d have lost your down payment. The 5x leverage works both ways. Such people weren’t as lucky as you and they do exist.

If prices stagnate and a renter saves more on housing than you pay in equity, at the end of your mortgage, they’d be able to buy your house with their savings and live just as comfortably without paying rental market prices.

So yeah, buying is a far better investment today, only if you bet it’s going to go up. And only if you make enough money (200K to comfortably support the below-median 740K scenario above) so that you’re able to absorb shocks without being forced to sell at an unfavorable time/price. It has been true for a while and if (when) interest rates fall, prices are likely to go up, but that would only happen because it would become cheaper to carry the higher mortgages required to inflate the prices further, because incomes are not rising nearly as fast.

In my opinion (and I think the article’s) buying today with lower income where you have little buffer left after paying those 5K is a recipe for disaster. I would rent when significantly cheaper than buying, buy when similar or cheaper than renting.

Flat since 2022… It’s barely 2024 and central banks had to increase interest rates by 4% due to inflation in that period. They’re now talking about dropping that interest rate and the real estate market is already salivating.

Your argument about buying at the peak and losing your job is not useful, of course it has some limited risk, but you’re talking about a few thousand people losing their down payment due to vs a few million making absolute bucket loads of money. You could get hit by a car tomorrow too, doesn’t mean you should make financial decisions based on that small potential that something bad will happen to you.

“If prices stagnate” - That’s a big If, historically speaking.

I’m 100% betting housing prices continue to rise, the government has no interest in actually decreasing the cost of housing from a political perspective. The majority of Canadian families own their own home, especially older Canadians who vote more frequently than younger people. They may try to keep it from going up so fast, but any growth is still going to make purchasing a better decision. It will not become politically viable to crash the housing market until home ownership rates drop 10-20% off current values, and that’s going to take decades.

I literally bet my house on this, We bought a home that’s significantly bigger than I need right now because I expect my three school aged children will not be able to move out in 10 years and will need to live at home with us for a significant amount of time. There’s even enough space on the property to build a secondary dwelling unit (and zoning allows this) for one of them to have their own home.

As I said, it’s a bet. You acknowledge that. I’m not betting but I’m looking at the situation today for someone who’d have to buy today, as is the article.

I don’t disagree with the political assessment however you’re missing some details that make your bet seem less risky. Which is totally alright since you’ve already made it. 😅

Speaking of people making boatloads of money, no one has made any money unless they bought a second property or are willing to downgrade. Anyone who’s only property has grown in price and they can’t afford to move to a cheaper one has made nothing except for their taxes have gone up. (Because they’d have to spend what they get for theirs on the one they have to buy, which has also gone up as much as theirs.)

What the hell are you doing at this house that you need $1000 in maintenance every month.

You can’t buy a house in the GTA for 700K. You’re buying a 2 or 3-bedroom condo for that much today. Check the maintenance fees for such units in the GTA. I don’t think you’d see much under $600 for a 2-bed and often without hydro/water/heat in it.

good thing I’m not living in Grand Theft Auto I guess

it is not that you pay that per month( unless you have strata building fees) but you have a roof replacement, or furnace change then you have a huge expense spread over you maintenamce saveing account. I once had Vaccum ,cleaner washer and dryer die in one week. But when I rented that is somebody elses problem. It was good renting 10 years ago maybe, but those days are done

$1k in maintenance is rather a lot.

Ours in 2 bedroom condo is about $450 to the strata for building maintenance, but then there are in unit maintenance like appliances breaking, etc

Not in my experience in the GTA. The cheapest all-inclusive maintenance I’m aware of is in the $600 area and that’s for 2-bedroom units in much, much worse building. Larger 3-bedrooms (1200-1500 sq.ft.) in decent buildings cost $800-$1200. Whenever I see cheaper maintenance for such units it typically doesn’t include hydro/water. Let alone Internet and cable.

it typically doesn’t include hydro/water. Let alone Internet and cable.

I have literally never lived anywhere that had included utilities. Nowhere I have ever rented in 24 years of renting has done literally any maintenance per month. It’s basically “Did you water heater explode?” They always use some family friend they pay 50 bucks to cut a hole in the wall, replace a plastic pipe, and then just screw in a cover over it.

Rather that renting can be significantly cheaper and less risky to your savings in the current market.

I can’t tell if you’re joking or not.

The value of owner-occupied homes grew by almost 40% between 2016 and 2021.

Get out of here with that ‘oh woe is the landlord’ garbage.

I don’t think you understand what I’m saying and what you cited here doesn’t contradict any of what I said. Perhaps I’m not explaining well enough. Back in 2016 I had no doubt that I would be buying if I had the money to.

those who own their home have been lucky enough to offset those costs by way of a significant increase in the value of their homes

That said this part is simply false for people who own just one property - the one they live in. If you own a 1-bedroom condo which went from 400K to 800K between 2016 and 2021 and want to take the difference, you have to sell it. Great, you have 400K extra. Now where would you live? Unless you’re moving to a less expensive area or downgrade (to … a studio?) you have to buy another 1-bedroom condo. Guess what, that also went from 400K to 800K between 2016-2021, so the extra 400K you made is gonna go to cover that. Price appreciation only makes money if you switch to living somewhere cheaper, in smaller property or a cheaper location; or if you buy an additional property that you rent.

Get out of here with that ‘oh woe is the landlord’ garbage.

We’re talking about what’s better for a person looking to house themselves via renting or buying, not sure what you’re going on about.

That said this part is simply false for people who own just one property - the one they live in. If you own a 1-bedroom condo which went from 400K to 800K between 2016 and 2021 and want to take the difference, you have to sell it. Great, you have 400K extra. Now where would you live?

I don’t know, but based on your previous comment where you said you’d save about $1700/mo renting you’d be 15 years of savings ahead of the renter.

My previous comment ($1700/mo) speaks of the status quo today and as I said in other comments it doesn’t bet whether the market would go up or down from here. It considers a sideways market.

The scenario where a condo doubles in price between 2016 and 2021 already has embedded in it the buyer winning the bet that the market would go up. I was merely clarifying the point that these savings aren’t realized unless the buyer changes accomodations for something cheaper, or as you point out, begins to rent. The article states it as if this money is available to spend when in the vast majority of cases it never becomes available.

Personally I did bet the market would go up back in 2016. If I have to bet today … I cannot picture how condos that were 400K in 2016, which are 800K today would become 1600K in 2031. We’re already at the point where the median household in Toronto has to pay 45% of its gross income to own the median condo, not a house. The median income has to increase significantly to sustain significant further growth in my opinion at this point. At 2% interest, the 45% number goes down to 32%, so lower interest rates are probably gonna pump it a bit higher, however inflation has already eaten up quite a bit of income so I think the effect would be softer than the typical.

My house has potentially increased in value almost $40k since I bought it almost two years ago. While most of my mortgage payments right now go towards interest. The equity I’ve gained by its value increasing is more than what the payments have done for me. I can’t realize that without selling, which I don’t intend to.

This works with a housing market that is flat. But somewhere like Vancouver your home equity goes up on its own year after year, and your rent scenario left over cash will never compete

It’s like the story of a Vancouver woman who lived in an apartment in English Bay. She was a server when she moved there 10 years ago, and had no issue affording it. Over the years she got settled, went to school while working and became a lawyer.

She eventually had to move out of the same apartment as it was no longer affordable, despite becoming a lawyer and earning significantly more money.

If she can’t keep pace with inflation going from a server to a lawyer, not sure what hope the rest of us would have.

I was making about 110,000 a year and gtfo of Vancouver in 2018. Saved way more money a year making 65-70 in south Alberta/Saskatchewan and now own my home outright.

As a young person, I love living astronomically.

Nice job with the headline quote, BNN Bloomberg writer.

Most of Europe rents, even people who make 6 figures and live in big cities…there’s absolutely no stigma attached to renting, in contrary people who decided to get a 35 year mortgage for an overpriced house (which often isn’t even a single house but a semi or a house with 3 ft of land around it) to live on the outskirts among conservative simpletons are thought of as suckers… It helps though that in the EU renters have rights and landlords are extremely limited in terms of raises or contract changes.

I’ve seen European Redditors say that European rental apartments tend to have better layouts and separation between units.

Probably better sound proofed too as they were built as multi units from the start instead of being a regular house renovated into apartments.

That’s what I was trying to get at with “separation”.

There’s nothing like since pax europa chad wandering into a Canadian housing discussion.

Apparently something to do with how stairwells are placed.

…and that the rental price isn’t 90% of the mortgage payment.

90%?

Oh my sweet summer child, rent is normally 150% of the mortgage.

Where?

Canada at least.

I can get a mortgage for an apartment for $1400 a month. Rent in the same spot would be at least $1800 if not $2000.

People buy housing to rent out because it’s profitable right away, they aren’t just “taking the risk” that the house might not go up in value.

deleted by creator

This is a bit of a fallacy. In a normal market, the rent for a home is less than the costs of home ownership (mortgage + maintenance + taxes) and that saved money can be used to purchase other assets.

Until the real estate mania of the last few years, if you followed this strategy, you would not be any worse off than the person who bought their home.

I personally would much rather have equity in more fungible assets than a home. Owning a home ties you to a specific location, and can’t easily be sold in an emergency. Plus it’s not a very diverse portfolio if most of you wealth is in a single property

If you can find such an asset for a fair price, then it might be a good investment, but that’s like hitting the lottery at the end of a bubble. There’s no guarantee your asset will rise in value or even just stay the same. It also depends on one’s financial situation. I pay about 15% of my net income on rent for nice flat in a modern building from 2021. If I could have the same living standard with a mortgaged asset for the same 15% of my net monthly income, I would consider buying, but it’s impossible even if I’d put down 25% cash upfront. House prices are crazy in Europe, I heard it’s due to all kinds of shady organisations like the Russian Mafia parking and washing their money here.

Only individuals should be able to buy and own residential property. Not corporations, not numbered companies, just people. They can rent them out, etc but don’t get the same protections of corporations. It becomes personal at that point. Banks generally will finance about 20 properties this way before they decide the liability becomes too much. This protects small landlords still, but gets all the big money out.

Then the rental market will price itself fairly based off of that and keep the rental market in check, but when the corporations own both sides of the coin they set the price.

Many of our MPs are landlords themselves, which may influence how… reactive they are to the issue https://www.landlordmps.ca/data-analysis

Our economy is over-reliant on housing as an investment in general, so getting people to do anything about it is hard to begin with https://www.oecd.org/housing/policy-toolkit/country-snapshots/housing-policy-canada.pdf

It’s not looking good. We’re in so deep already. A lot of people will lose their homes either way.

This is why I avoid REITs and housing investment like the plague. It’s a house of cards.

multiple degrees. established in my industry. “well paid” among my peers… Renovicition means I’m living with my parents in my 30’s. This is madness.

Exact same situation. 29 making over six figures and renoviction means back to my parents or sleeping on the street

As someone making roughly half of 100k per year. I can afford my small apartment, to shop wisely for food, and carpool to work and with that I manage to save 1000 or more a month. I don’t know the specifics of your situation but you should still be able to live on your own with a 100k salary.

It entirely depends on where you live.

Out in the sticks where the opportunities are few, the cost of living is way lower.

I live in Victoria

Canada has become such a shithole and I can’t wait to get out

If you’re young, pretty much everywhere is a shit hole nowadays.

Pretty much except Iceland and Finland

PS if you’re younger than 31 you can get the youth mobility visa to work in Iceland, that started only a few months ago, which is what I’m planning on utilizing

Only open to so many applicants per year, so hopefully you get in. Happiest rating, but also somehow most murders…maybe those correlate

Iceland… Murders? No lol

New Zealand seems to be just fine too.

Nah worse housing mess than us

It’s absolute shit for young people and anyone who doesn’t own a home already. Pants on head insane house prices for cardboard walls and mould. Violent crime and especially gang crime is straight up scary now (though not as bad as the bad parts of America). I left NZ because my outlook was so bleak. I ended up in Denmark and couldn’t be happier. Australia is also a good bet and the women are GORGEOUS. Also Switzerland if you find a path to employment there. Norway is great. Many places in America are still great, despite the counter-jerk.

…and go where exactly?

Things are not easy here but unless you are buying into the Conservative narrative that even the bad weather is Trudeau’s fault, “getting out” is not really a better option…

Iceland via youth mobility visa

Alternately my sister in law lives in Finland so have a couple different options

Wow you’re lucky! One of the few countries that treat people well.

Well I haven’t been accepted yet but fingers crossed! They are still processing visas from summer 2023 so I won’t know for quite a while

Hmm I’m sure a 12 month change of scenery would be great… Not sure how that will change your prospects in the mid term

Should be able to get 24 months, hopefully long enough to find an employer willing to sponsor me permanently

Best of luck bud

Thanks I’ll need it

deleted by creator